Explore our collection of free tools and calculators to make informed decisions.

Explore All ToolsYour trusted hub for free calculators and tools. We make financial planning simple and accessible for everyone.

Tools & Calculators

Calculations

Fast Results

Trusted

Calculate income tax on salary India FY 2025-26: new regime slabs, TDS projection, mid-year increment, bonus spike & professional tax by state explained.

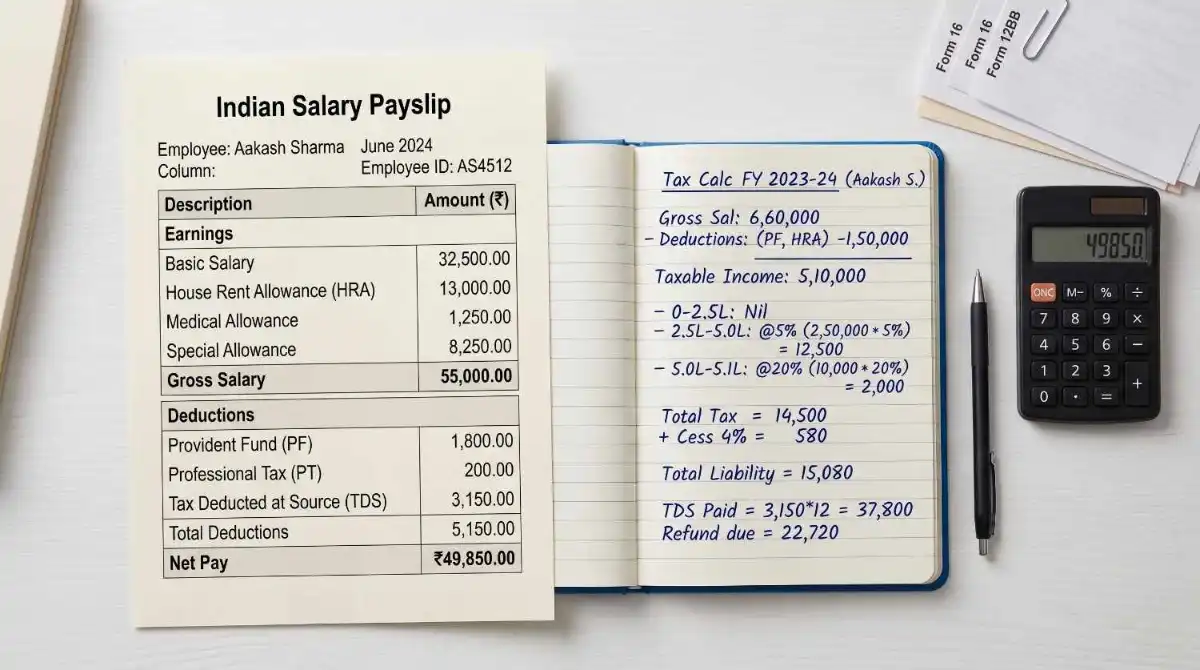

Your income tax on salary for FY 2025-26 (Assessment Year 2026-27) equals your taxable salary — after the ₹75,000 standard deduction under the new regime — passed through seven progressive slabs under Section 115BAC of the Income-tax Act, 1961, then reduced by a rebate of up to ₹60,000 under Section 87A if your taxable income is ₹12 lakh or below, and a 4% Health and Education Cess added on the final figure. If your employer's TDS looks wrong every month, it isn't a mistake — this guide explains exactly why and how to check it.

Income tax on salary is the direct tax levied by the Central Government on your income under the head "Salaries," computed under the Income-tax Act, 1961 (Section 15 onwards) and deducted monthly by your employer as Tax Deducted at Source (TDS) under Section 192. For FY 2025-26, the new tax regime under Section 115BAC is the default; you must actively opt out to use the old regime. The new regime replaced "Previous Year" and "Assessment Year" terminology only in the Income-tax Act, 2025, which governs Tax Year 2026-27 onwards — FY 2025-26 income is still assessed under the 1961 Act.

Applies To | Does NOT Apply To |

|---|---|

Salaried employees (private, government, PSU) | Self-employed individuals with no salary income |

Pensioners (pension is taxed as salary) | Partners drawing only profit share from a firm |

Employees paid salary by a foreign employer inside India | NRIs earning salary solely outside India |

Employees who receive salary arrears or advance salary | Freelancers with only professional fees (different head) |

Part-time employees with a salary slip | Individuals earning below ₹4 lakh (zero tax, new regime) |

Partial/conditional: If you earn salary from two employers simultaneously in the same FY, both must deduct TDS under Section 192 — but only if each employer is informed of the other's salary. If they are not, you will have a shortfall and a tax demand at filing.

New Tax Regime (Section 115BAC — default from FY 2023-24)

Taxable Income | Tax Rate |

|---|---|

Up to ₹4,00,000 | Nil |

₹4,00,001 – ₹8,00,000 | 5% |

₹8,00,001 – ₹12,00,000 | 10% |

₹12,00,001 – ₹16,00,000 | 15% |

₹16,00,001 – ₹20,00,000 | 20% |

₹20,00,001 – ₹24,00,000 | 25% |

Above ₹24,00,000 | 30% |

Key deductions allowed under new regime:

Standard deduction: ₹75,000 (Section 16(ia))

Employer NPS contribution: up to 14% of basic salary (Section 80CCD(2))

Section 87A rebate: 100% of tax, capped at ₹60,000, for taxable income up to ₹12 lakh

Health & Education Cess: 4% on tax after rebate

Old Tax Regime (Section 115BAC(6) — must opt in): Slabs: ₹0–₹2.5L = nil; ₹2.5L–₹5L = 5%; ₹5L–₹10L = 20%; above ₹10L = 30%. Standard deduction: ₹50,000. Full deductions under 80C (₹1.5L), 80D, HRA exemption, LTA available.

Step 1 — Find your gross salary. Add basic pay + HRA + DA + all allowances + bonuses for the full year.

Step 2 — Subtract exemptions (old regime only). HRA exemption under Section 10(13A), LTA under Section 10(5). Under the new regime, skip this step.

Step 3 — Apply standard deduction. Deduct ₹75,000 (new regime) or ₹50,000 (old regime) under Section 16(ia).

Step 4 — Subtract other deductions. New regime: only 80CCD(2) employer NPS contribution. Old regime: 80C up to ₹1.5L, 80D, 80E, 80TTA, etc.

Step 5 — This is your taxable income. Apply the slab rates from the table above.

Step 6 — Apply Section 87A rebate. If taxable income is ₹12 lakh or below (new regime) or ₹5 lakh or below (old regime), subtract the rebate from the slab tax.

Step 7 — Add 4% cess. Multiply total tax after rebate by 1.04.

Step 8 — Add surcharge if applicable. Taxable income above ₹50 lakh: 10% surcharge on tax.

Suresh earns ₹15,00,000 gross salary annually. He has no other income and opts for the new regime.

Step | Calculation | Amount |

|---|---|---|

Gross Salary | — | ₹15,00,000 |

Less: Standard Deduction (Sec 16(ia)) | — | ₹75,000 |

Taxable Income | — | ₹14,25,000 |

Tax on ₹0–₹4L | Nil | ₹0 |

Tax on ₹4L–₹8L | 5% of ₹4,00,000 | ₹20,000 |

Tax on ₹8L–₹12L | 10% of ₹4,00,000 | ₹40,000 |

Tax on ₹12L–₹14.25L | 15% of ₹2,25,000 | ₹33,750 |

Total slab tax | — | ₹93,750 |

Section 87A rebate | Taxable income > ₹12L — not eligible | ₹0 |

4% Cess | 4% of ₹93,750 | ₹3,750 |

Annual Tax | — | ₹97,500 |

Monthly TDS (April) | ₹97,500 ÷ 12 | ₹8,125 |

Priya earns ₹12,75,000 gross salary. She opts for the new regime.

Step | Amount |

|---|---|

Gross Salary | ₹12,75,000 |

Less: Standard Deduction | ₹75,000 |

Taxable Income | ₹12,00,000 |

Slab tax on ₹12L | ₹0 + ₹20,000 + ₹40,000 = ₹60,000 |

Section 87A rebate (100%, capped ₹60,000) | -₹60,000 |

Net Tax | ₹0 |

Priya pays zero income tax. The ₹75,000 standard deduction is what pushes her taxable income to exactly ₹12 lakh and qualifies her for the full ₹60,000 rebate.

Every month your employer calculates TDS using a 12-month projection method under Section 192. At the start of the year, your employer estimates your total annual taxable income, calculates the full-year tax, then divides by the remaining months.

Why it changes: When you submit investment declarations in April, your employer projects a lower annual tax and spreads it over 12 months. When you submit actual investment proofs in January, the employer recalculates — if you claimed ₹1.5L under 80C but only invested ₹80,000, the shortfall is recovered over the remaining months.

Concrete example — Ramesh, ₹12 LPA:

April projection (no investment proof submitted): Annual tax = ₹60,000 − rebate = ₹0. Monthly TDS = ₹0. Wait — but Ramesh's salary is ₹12L gross, taxable income is ₹12L − ₹75,000 = ₹11.25L. Slab tax: ₹0 + ₹20,000 + ₹32,500 = ₹52,500. Cess: ₹2,100. Annual tax = ₹54,600. Monthly TDS in April = ₹54,600 ÷ 12 = ₹4,550.

October — Ramesh gets ₹50,000 performance bonus: Revised annual income = ₹12,50,000. Taxable = ₹11,75,000. Tax = ₹0 + ₹20,000 + ₹37,500 = ₹57,500 + cess ₹2,300 = ₹59,800. Already deducted April–September: ₹4,550 × 6 = ₹27,300. Remaining tax = ₹59,800 − ₹27,300 = ₹32,500 over 6 months = ₹5,417/month from October.

That's why Ramesh's February TDS is higher than his April TDS even if his salary didn't change — the bonus adjusted the projection.

When your salary hikes mid-year, your employer recalculates the annual projection using actual months at old salary plus projected months at new salary. The entire revised tax minus what was already deducted must be recovered over the remaining months.

Example — Farida, ₹10 LPA → ₹14 LPA (October hike), New Regime:

Old salary period: April–September (6 months) at ₹10 LPA = ₹5,00,000 New salary period: October–March (6 months) at ₹14 LPA = ₹7,00,000 Projected annual income: ₹5,00,000 + ₹7,00,000 = ₹12,00,000 Taxable income: ₹12,00,000 − ₹75,000 = ₹11,25,000

Slab | Tax |

|---|---|

₹0–₹4L | ₹0 |

₹4L–₹8L | ₹20,000 |

₹8L–₹11.25L | ₹32,500 |

Total slab tax | ₹52,500 |

4% Cess | ₹2,100 |

Annual tax | ₹54,600 |

TDS already deducted April–September (6 months at ₹10L rate): Old annual tax (₹10L gross): Taxable = ₹9,25,000. Slab: ₹0 + ₹20,000 + ₹12,500 = ₹32,500 + cess ₹1,300 = ₹33,800. Monthly TDS = ₹33,800 ÷ 12 = ₹2,817. Deducted so far: ₹2,817 × 6 = ₹16,900.

Remaining tax to collect: ₹54,600 − ₹16,900 = ₹37,700 over 6 months (October–March) = ₹6,283/month.

Before the hike, Farida's TDS was ₹2,817. After October, it becomes ₹6,283 — more than double — and it feels like a salary cut even though her gross went up. This is normal and correct.

When you join a new employer mid-year, the new employer has no record of what your previous employer paid you or deducted as TDS. Without that information, the new employer starts the annual projection from scratch using only your new CTC.

What this means: Your new employer assumes you earned nothing before joining them. They calculate annual tax only on your new salary — which is artificially low. TDS for the first few months at the new employer will be low. Then, when the financial year is almost over, the gap closes suddenly and TDS spikes in January–March.

The fix: Form 12B. Under Rule 26A of the Income Tax Rules, 1962, you must submit Form 12B to your new employer when joining. It contains your previous employer's salary details, TDS deducted, and PAN. Your new employer adds the two together to compute the correct annual projection.

What happens if you skip Form 12B: The new employer underdeducts TDS. At ITR filing, you'll owe the shortfall as tax plus interest under Section 234B for self-assessment tax shortfall.

Example — Ramesh, April–August at ₹8 LPA (₹3.33L), joins new company September at ₹13 LPA:

Annual projection WITH Form 12B: Previous salary: ₹3,33,333 (5 months at ₹8L rate) New salary: ₹7,58,333 (7 months at ₹13L rate) Total projected income: ₹10,91,667 Taxable: ₹10,91,667 − ₹75,000 = ₹10,16,667 Tax: ₹0 + ₹20,000 + ₹21,667 = ₹41,667 + cess ₹1,667 = ₹43,333 TDS deducted April–August by old employer (say ₹8,000): ₹8,000 × 5 = ₹40,000 Remaining: ₹43,333 − ₹40,000 = ₹3,333 over 7 months = ₹476/month from new employer.

WITHOUT Form 12B (new employer only sees ₹13 LPA): New employer projects: ₹13L × 7/12 months (Sep–Mar) ≠ correct. They calculate as if Ramesh earns ₹13L for the full year: taxable = ₹12,25,000. Annual tax ≈ ₹78,750 + cess ₹3,150 = ₹81,900. Divided over 7 months: ₹11,700/month — a sudden shock in September.

Submit Form 12B on Day 1 at your new employer. Ask HR for the form; provide your old employer's name, TAN, salary breakup, and TDS deducted certificate.

Three things happen between October and January that reset TDS calculations:

1. Investment proof deadline. Most employers require you to submit actual investment proofs (80C instruments, insurance, school fees receipts) by December or January. If you declared ₹1.5L under 80C in April but submit proofs for only ₹80,000, the employer removes the ₹70,000 unproven deduction. Your taxable income rises retroactively for the full year, and the extra tax is collected over the remaining months.

2. Diwali or year-end bonus. A one-time bonus credited in October temporarily spikes projected annual income (see Bonus Month section below). Even if the spike reverses in November, the adjustment plays out across December–March.

3. Year-end convergence. By January, only 3 months remain. Any shortfall in TDS across the prior 9 months must be cleared in those 3 months. This is mathematical, not a penalty — your employer is simply ensuring the full-year tax is deducted before March 31.

Your action: Submit investment proofs as soon as you have them — don't wait until December. If you submit by October, your employer can spread the adjustment over more months.

When a bonus is credited in a single month, your employer treats that month's total pay (salary + bonus) as if it repeats every month. This inflates the annual projection for one calculation cycle. The following month, the projection resets to normal salary — but the extra TDS already deducted stays deducted, often causing the next month to show lower TDS to compensate.

Example — Vikas, ₹12 LPA + ₹1 lakh Diwali bonus in October:

Normal monthly TDS (₹12L gross as above): ₹4,550/month.

October pay = ₹1,00,000 salary + ₹1,00,000 bonus = ₹2,00,000 in that month. Annual projection for October: ₹2,00,000 × 12 = ₹24,00,000 gross. Taxable: ₹24,00,000 − ₹75,000 = ₹23,25,000. Slab tax: ₹0 + ₹20,000 + ₹40,000 + ₹60,000 + ₹80,000 + ₹75,000 + ₹97,500 = ₹1,07,500 (on ₹23.25L). Wait — slab recalculation on ₹23.25L: up to ₹4L nil; ₹4–8L = ₹20K; ₹8–12L = ₹40K; ₹12–16L = ₹60K; ₹16–20L = ₹80K; ₹20–23.25L = 25% × ₹3.25L = ₹81,250. Total = ₹2,81,250 + cess ₹11,250 = ₹2,92,500. Already deducted April–September (6 × ₹4,550): ₹27,300. Remaining: ₹2,92,500 − ₹27,300 = ₹2,65,200 over 6 months = ₹44,200/month.

That ₹44,200 October TDS feels catastrophic. In November, when the employer recalculates with ₹12L normal salary, the over-deduction adjusts downward and TDS drops below normal.

Can you ask your employer to spread TDS? Yes. Section 192(2B) allows employees to declare other income or losses to their employer, and employers can adjust TDS projections. Ask your payroll team in writing to distribute the bonus TDS across remaining months rather than taking it all in the bonus month. Not all companies accommodate this — it is at the employer's discretion.

If you suspect your TDS is wrong, here are the exact steps to check:

Step 1 — Get your salary slip. Note gross salary, all allowances, and TDS deducted for the month.

Step 2 — Calculate your own taxable income. Take your annualised gross salary (monthly × 12 or actual YTD + projected remaining months). Subtract ₹75,000 standard deduction. Subtract any 80CCD(2) employer NPS contribution you have submitted to your employer.

Step 3 — Apply FY 2025-26 new regime slabs. Calculate annual tax using the table in Section 3 above. Divide by 12 (or by remaining months if mid-year).

Step 4 — Compare with your salary slip TDS. If your calculated TDS differs by more than ₹500/month, something may be off. Common errors: employer applied old regime when you chose new; employer missed the ₹75,000 standard deduction; employer did not include a previous employer's salary (if you switched jobs and submitted Form 12B).

Step 5 — Cross-check Form 26AS / AIS. Log in to incometax.gov.in, go to "e-File → Income Tax Returns → View Form 26AS" (now also accessible as Annual Information Statement under AIS). Your employer's TDS deposits appear here by quarter. If the amount your employer claims to have deducted is not visible in Form 26AS, the employer may not have deposited it — which is an employer default, not your liability, but it will affect your ITR.

Use Toolisky's free salary tax calculator to verify your own TDS in under 60 seconds — enter your gross salary, regime, and NPS contribution to get the correct annual tax and monthly TDS figure.

Professional tax (also called Employment Tax) appears on every Indian salary slip but varies sharply by state. It is a state-level tax under Article 276 of the Constitution, capped at ₹2,500/year.

Key rule on deductibility: Professional tax is deductible from salary income only under the old tax regime (Section 16(iii)). Under the new regime (Section 115BAC), professional tax is not deductible. If you are in Maharashtra and on the new regime, your ₹2,500/year professional tax is NOT subtracted when computing your taxable income.

State | Annual Professional Tax | Monthly Deduction Pattern |

|---|---|---|

Maharashtra | ₹2,500 | ₹200/month (Feb ₹300) |

Karnataka | ₹2,400 | ₹200/month |

West Bengal | ₹2,400 | Varies by income slab |

Tamil Nadu | ₹2,400 | ₹200/month |

Andhra Pradesh | ₹2,400 | Varies by slab |

Telangana | ₹2,400 | Varies by slab |

Gujarat | ₹2,500 | ₹208/month |

Madhya Pradesh | ₹2,500 | Varies |

Delhi | ₹0 | No professional tax |

Rajasthan | ₹0 | No professional tax |

Haryana | ₹0 | No professional tax |

Uttar Pradesh | ₹0 | No professional tax |

Uttarakhand | ₹0 | No professional tax |

Himachal Pradesh | ₹0 | No professional tax |

[VERIFY: Confirm exact professional tax slab amounts and threshold income levels for West Bengal, Andhra Pradesh, Telangana, and MP — state government gazette notifications. Check: wbfinanace.gov.in / apts.gov.in / tgct.gov.in / mpfinance.gov.in]

A common misconception: employees in Delhi often see no professional tax line on their payslip and assume it was forgotten. Delhi has no professional tax legislation — zero is correct.

Scenario 1: TDS deducted but not deposited by employer. Symptom: Your salary slip shows TDS, but Form 26AS shows a lower amount or nothing. This is the employer's default under Section 201. Your action: do not panic — you are not liable for the employer's failure to deposit. File your ITR showing TDS as per your salary slip/Form 16. Attach a declaration explaining the mismatch. The Income Tax Department will pursue the employer. If you receive a demand notice, respond via the portal under "Respond to Outstanding Demand" and submit your Form 16 as evidence.

Scenario 2: Wrong tax regime applied by employer. Symptom: You submitted Form 10IEA to opt for old regime but employer deducted TDS as per new regime (or vice versa). Your action: submit a written request to your HR/payroll citing Section 192(2C), which requires employers to take into account the employee's regime declaration. Ask for a revised TDS computation. If the financial year has ended, file your ITR under the correct regime — the regime elected at ITR is final for non-business taxpayers under Section 115BAC(6).

Scenario 3: TDS mismatch causes a tax demand after filing. Symptom: After filing ITR, you receive an intimation under Section 143(1) showing tax payable because TDS on Form 26AS doesn't match your declared TDS. Your action: first verify Form 26AS carefully. If the mismatch is the employer's non-deposit (Scenario 1), file a rectification request under Section 154 through the portal. If it's a genuine underpayment, pay the shortfall immediately using Challan 280 online at incometax.gov.in to avoid Section 234B interest (1% per month on shortfall).

Default | Penalty / Interest | Section (1961 Act) |

|---|---|---|

Late filing of ITR (income above ₹5L) | ₹5,000 | Section 234F |

Late filing of ITR (income up to ₹5L) | ₹1,000 | Section 234F |

Filing after 31 Dec 2026 (belated return) | ₹5,000 + 1% interest/month | Section 234A + 234F |

Shortfall in advance tax payment | 1% per month on shortfall | Section 234B |

TDS shortfall (employer) | Equal to TDS amount not deposited | Section 201(1A) |

Concealment of income | 100%–300% of tax evaded | Section 270A |

Non-filing if income above threshold | Prosecution possible | Section 276CC |

ITR due date for FY 2025-26 (AY 2026-27) for salaried non-audit cases: 31 July 2026.

1. How do I calculate income tax on a ₹10 lakh salary for FY 2025-26? Gross salary ₹10,00,000 minus ₹75,000 standard deduction = taxable income ₹9,25,000 under the new regime. Tax: ₹0 (up to ₹4L) + ₹20,000 (₹4–8L at 5%) + ₹12,500 (₹8–9.25L at 10%) = ₹32,500 plus 4% cess = ₹33,800 annually. Monthly TDS = ₹2,817. You are not eligible for the Section 87A rebate because taxable income exceeds ₹12L threshold — wait, ₹9.25L is below ₹12L, so rebate IS available: ₹33,800 is under ₹60,000 → full rebate. Net tax = ₹0. Your ₹10L salary is completely tax-free under the new regime.

2. Is a ₹12 lakh salary really tax-free? Yes, with one condition. Gross salary ₹12L minus ₹75,000 standard deduction = ₹11.25L taxable income. Tax on ₹11.25L = ₹52,500 + cess ₹2,100 = ₹54,600. The Section 87A rebate caps at ₹60,000 and covers any tax up to ₹12L taxable income. Since ₹54,600 < ₹60,000 and taxable income is ₹11.25L < ₹12L, the full tax is waived. But if your gross is ₹12L and you have additional income (FD interest, capital gains), that extra income may push taxable income above ₹12L and the rebate disappears entirely.

3. My TDS was zero in April but jumped in January. Did my employer make a mistake? Almost certainly not. If you submitted investment declarations in April (claiming HRA, 80C, etc.) but submitted incomplete or no proofs by December, your employer added back the unverified deductions and recalculated tax. The shortfall of 9 months is recovered in the remaining months. This is legally correct under Section 192.

4. What is the standard deduction for salaried employees in FY 2025-26? ₹75,000 under the new regime (Section 16(ia), as amended by Finance (No. 2) Act, 2024). ₹50,000 under the old regime. No receipts or proofs required. It is deducted automatically by your employer.

5. Can I switch between old and new regime every year? Yes, if you are a salaried employee without business income. You can change your regime at ITR filing time, without any form, every year. If you have income from business or profession, you must file Form 10-IEA and the switch is limited — you get only one chance to re-enter the new regime.

6. My Form 26AS shows less TDS than my salary slip. What should I do? Your employer deducted TDS from your salary but has not deposited it with the government. File your ITR based on the amount shown on your Form 16 (not just Form 26AS). If you receive a Section 143(1) demand, submit a rectification with your Form 16. The employer is liable under Section 201(1A) — not you.

7. I joined a new company in September. Should I submit Form 12B? Yes, on your first day. Without Form 12B, your new employer does not know about the salary and TDS from your previous employer. They will underdeduct TDS for the first few months, then spike it in January–March to compensate. Worse, if total underdeduction exists at year-end, you pay the balance as self-assessment tax plus interest under Section 234B.

8. Is the Diwali bonus fully taxable? Yes. All bonuses — performance, annual, joining, referral, Diwali — are fully taxable as salary income under the head "Salaries." There is no exemption for bonus income under either regime. The tax effect on your payslip looks large because your employer's TDS projection for that month is calculated as if you earn that bonus every month (annualised), but it normalises in subsequent months.

9. Does professional tax reduce my income tax? Only if you opt for the old regime. Under Section 16(iii), professional tax paid is deductible from gross salary before computing income tax in the old regime. Under the new regime, this deduction is not allowed. A salaried employee in Maharashtra paying ₹2,500/year professional tax and using the new regime cannot claim it as a deduction anywhere.

10. What if I missed the ITR deadline of 31 July 2026? You can file a belated return up to 31 December 2026 under Section 139(4) with a late fee of ₹5,000 (or ₹1,000 if your taxable income is below ₹5L). After 31 December, you can file a belated return up to 31 March 2027 with ₹5,000 late fee plus interest under Section 234A at 1% per month on outstanding tax. You lose the right to carry forward most losses (except house property loss) if you miss 31 July.

11. My employer used the old regime but I wanted the new regime. Can I change at ITR? Yes. Your employer's regime choice does not bind you for the ITR. File your ITR under the new regime. The government will recalculate your tax, and if you have an excess TDS credit, you receive a refund. For future months, inform your employer in writing of your regime choice — they must honour it under Section 192(2C).

12. What is the exact ITR filing due date for FY 2025-26? 31 July 2026 for salaried individuals (non-audit cases) under Section 139(1).

Check your taxable income, apply the new regime slabs, subtract the Section 87A rebate if eligible, and compare the result with your salary slip TDS today. If you switched jobs this year, submit Form 12B immediately. Use Toolisky's free salary tax calculator to verify your exact numbers in under 60 seconds. For official slab tables and Form 26AS, visit incometax.gov.in.

For educational purposes only. Verify all figures at official sources before acting. Toolisky is not affiliated with any government body. Consult a qualified CA or legal professional before making compliance decisions. See toolisky.com/accuracy-and-limitations.

TDS rate chart FY 2026-27: All Section 393 rates, old-vs-new section mapping, 3 rate changes, payment due dates & worked ₹ examples. Updated July 2026.

Crypto tax India 2026 explained: 30% VDA tax, 1% TDS, new 18% GST, penalties, and whether the 1961 or 2025 Income Tax Act governs your crypto filing this year.

Jul 15, 2026

Form 8840 closer connection exception explained: SPT formula, Part IV walkthrough, 2025-26 deadlines, documents, and two real day-count examples.

Jul 15, 2026